The long-term cooperative credit structure, comprising State Cooperative Agriculture and Rural Development Banks (SCARDBs) and Primary Cooperative Agriculture and Rural Development Banks (PCARDBs), witnessed a sharp erosion in profitability in FY2023-24, with more banks slipping into losses and asset quality stress remaining severe.

Both sets of institutions reported weak performance during the year, swinging into losses while continuing to struggle with very high levels of non-performing assets (NPAs).

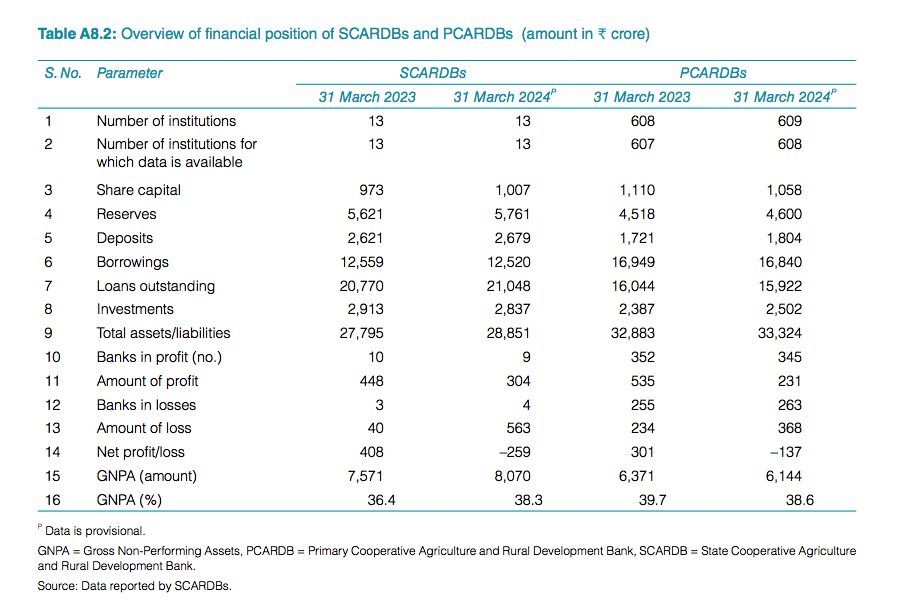

Spread across 13 states and Union Territories, these banks operate under three models- unitary, federal, and mixed. However, their financial indicators show increasing strain.

The number of loss-making banks rose, with SCARDBs increasing from three to four and PCARDBs from 255 to 263. Gross NPAs remained worryingly high at 38.3% for SCARDBs and 38.6% for PCARDBs in FY24.

On the balance sheet side, borrowings stood at Rs 12,520 crore for SCARDBs and Rs 16,840 crore for PCARDBs, while loans outstanding were reported at Rs 21,048 crore and Rs 15,922 crore, respectively. Total assets grew only marginally, with SCARDBs at Rs 28,851 crore and PCARDBs at Rs 33,324 crore.

Experts caution that the inherent structural limitations of these banks add to their financial vulnerability. Since they are not governed by the Banking Regulation Act, 1949, they cannot mobilise demand deposits from non-members, and such deposits are not covered under the Deposit Insurance and Credit Guarantee Scheme.

The combination of mounting losses and persistently high NPAs underscores the urgent need for reforms, stronger recovery mechanisms, and improved governance in the long-term cooperative credit sector.